Interest on loans: it’s one of those financial concepts we all think we understand but rarely stop to question. As someone who’s spent time in the lending business, I’ve often wondered at the nature of interest. Before a loan exists, interest doesn’t exist either. Yet, once the agreement is made, voilà-it appears, conjured up out of thin air. So, could it be argued that interest is, in essence, “fairy money”-an entirely invented cost, albeit one with some practical justifications?

Let’s dive into this idea and pick apart the mechanics and the rationale behind interest.

The “Making Up” of Interest

When I worked in the lending industry lending actual money, the process of setting interest rates was frankly, a bit arbitrary. There wasn’t some mystical formula we followed; it was a mix of market competition, perceived risk and crucially, profit margins. In simple terms, we made it up.

Now that’s not to say there weren’t legitimate factors at play. Lenders have to cover costs, account for risks and of course, make a profit. But the reality is, interest doesn’t pre-exist the loan-it’s added on top. It’s a number that emerges out of a lender’s goals and the borrower’s ability (or inability) to repay. And yes, sometimes it does feel like magic.

Why Interest Exists

While it may seem a bit “made up,” interest does serve a purpose. Let’s look at the three main reasons it exists:

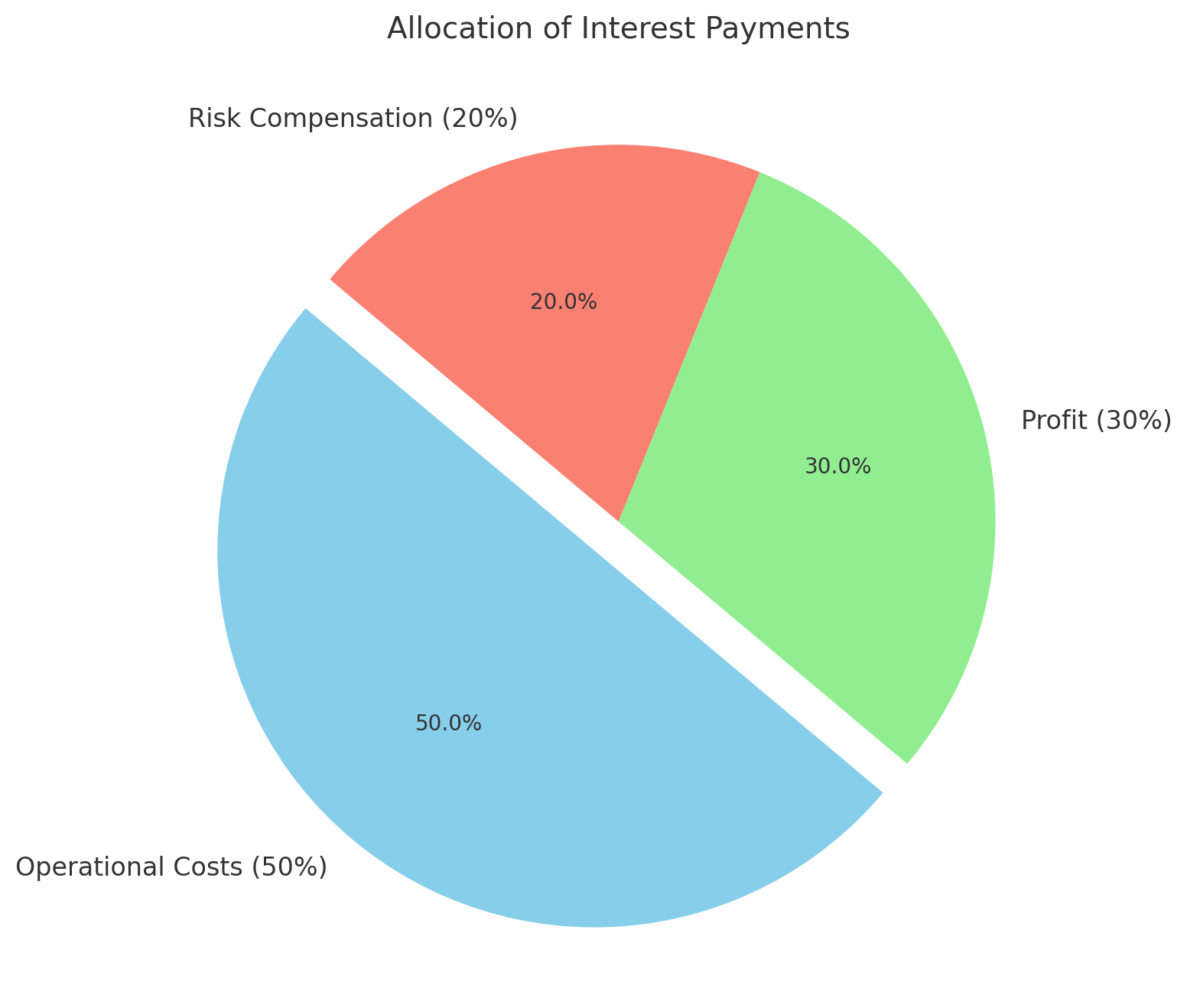

1. Compensation for Risk

When lenders give out loans, they take on the risk that borrowers might not repay. Interest is the price of that risk. However, the way risk is calculated feels more like educated guesswork than hard science. For example, borrowers with lower credit scores are charged higher rates, even if their actual likelihood of defaulting might not warrant it.

As someone who had their fair share of credit ‘issues’ back in the day it always struck me as particularly unfair that poor little old (young) me had to pay what seemed like exorbitant rates of interest because my risk was high for non-repayment when ‘rich’ people, that’s everyone else, were paying single digit rates of interest. How can that be, I wondered? Surely lenders wanted to help people like me get on the credit ladder by giving out cheap rate loans they could afford to repay. After all, we’re in debt for life these days so why not make getting on that ladder, a little bit easier?

It was also a mystery to young me why, when I had a bit of money in my bank account, banks, credit card and loan companies were falling over themselves offering to lend me money but when I desperately needed it nobody would look twice and I couldn’t raise 5p.

Sometimes it’s a long road to learning how the financial world works.

2. Time Value of Money

The time value of money is a cornerstone of finance. It’s the idea that £1 today is worth more than £1 tomorrow because it can be invested and earn more money. Interest is how lenders justify the cost of giving up their funds for a period of time. Still, this doesn’t change the fact that interest is an entirely constructed concept-it doesn’t exist until we create it.

3. Operational Costs and Profit

Lenders have bills to pay too. Staff salaries, office space, compliance costs-these all have to come from somewhere. Interest helps cover these costs and provides the all-important profit margin. This is perhaps the most tangible justification for interest-it keeps the business running.

The Loan Creation Process

1. Borrower Application

- The borrower submits a loan application, providing personal and financial details such as income, employment status, credit history, and desired loan amount.

2. Credit Assessment

- The lender assesses the borrower’s creditworthiness using:

- Credit score checks.

- Verification of income and expenses.

- Evaluation of loan purpose (if applicable).

- Automated systems or underwriters may handle this step.

3. Risk Assessment

- The lender evaluates the risk of lending to the borrower, factoring in:

- Likelihood of repayment.

- Potential default rates for borrowers with similar profiles.

- This analysis informs the interest rate offered.

4. Loan Offer

- Based on the risk assessment, the lender presents the borrower with:

- Loan terms (amount, duration, repayment schedule).

- Interest rate and any applicable fees.

5. Borrower Agreement

- If the borrower accepts the terms, they sign the loan agreement, which includes:

- Full disclosure of repayment obligations.

- Regulatory compliance details (e.g., cooling-off period or prepayment options).

6. Fund Disbursement

- The agreed loan amount is transferred to the borrower’s bank account, minus any upfront fees (if applicable).

7. Repayment Management

- The borrower begins repayment as per the agreed schedule. Repayments include:

- Principal amount.

- Interest (and any applicable fees).

- Payments are typically made via direct debit or standing order.

8. Monitoring and Collections

- The lender monitors repayment performance. If the borrower misses payments:

- Automated reminders are sent.

- Collections efforts are initiated (e.g., contacting the borrower, offering repayment plans).

- Persistent non-payment may result in escalation to debt recovery agencies. Default notices can be attached to credit files making it far harder to obtain credit.

9. Loan Closure

- Once all repayments are made, the loan account is closed. The borrower may receive:

- A final statement of account.

- An updated credit report reflecting successful repayment.

The “Fairy Money” Perspective

By looking at the above lending process we can see why lenders charge interest. They have an awful lot of Ts to cross and Is to dot both before and after releasing funds for your loan. So, if we accept that interest is essentially invented, does that make it inherently unfair? Not necessarily. Like many constructs in modern finance, it’s a tool-one designed to facilitate borrowing and lending. But the “fairy money” idea does raise some interesting questions:

1. How Transparent Is the Process?

Borrowers rarely understand how interest rates are determined. Could greater transparency demystify the process and foster trust?

2. Is Interest Always Justified?

In some cases, interest rates seem predatory, particularly in sectors like payday lending or for borrowers with poor credit. For readers interested in regulatory protections, the FCA’s rules on payday lending (https://www.fca.org.uk/) provide valuable insights into how these practices are governed. This is where the “fairy money” critique feels particularly sharp.

3. Who Benefits Most?

While lenders gain from interest, borrowers often bear the brunt of its costs. The “fairy money” perspective underscores how interest can exacerbate financial inequalities. The primary beneficiaries? The people who own the lending companies, their shareholders and directors. In short, the usual suspects.

However, how about the person who borrowed £5,000, took it and created something with value that produced something worthwhile that benefitted others around them as well as themselves and ultimately turned it into many times £5,000. That’s who we’re in business for.

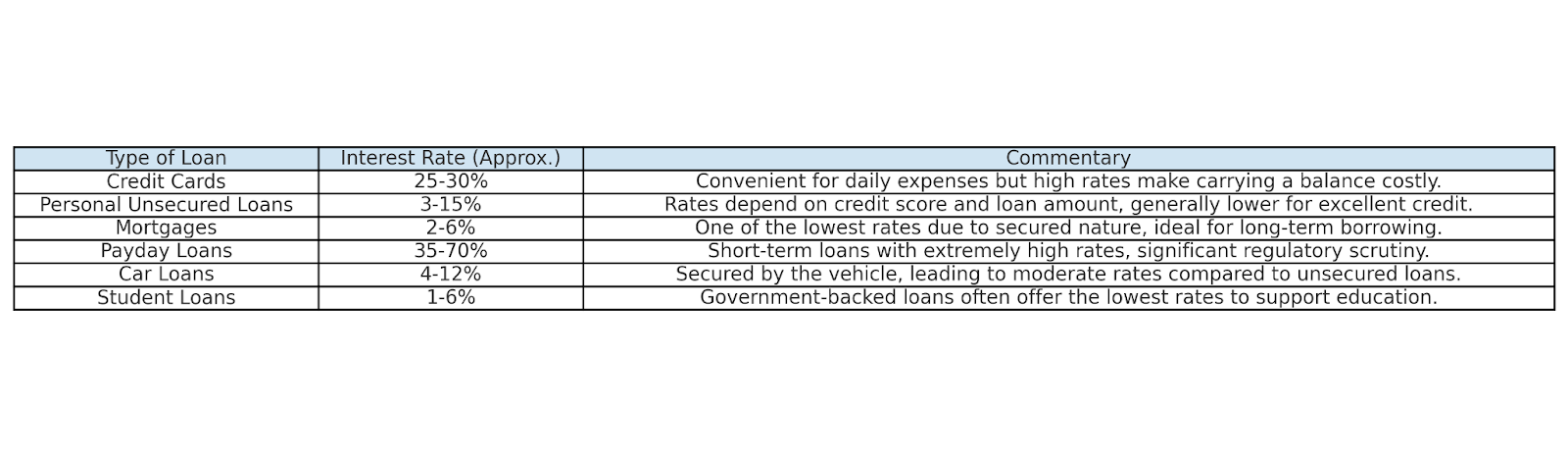

A comparison of average interest rates for various loan types.

Notes for Borrowers:

- These ranges provide general guidance but don’t account for fees or other charges that may increase the effective borrowing cost.

- Representative APRs are advertised but not guaranteed; individual offers may vary.

- Payday loans and unauthorised overdrafts can lead to spiralling costs if not repaid promptly. Never take out another payday loan before repaying the first one completely.

A New Way to Think About Interest

Interest might seem like an inevitable part of borrowing, but it’s worth remembering it’s not a natural law. It’s a construct – a number lenders create to make lending worth their while, balancing risk, costs, and profits. Understanding this “fairy money” nature of interest doesn’t diminish its importance, but it does invite us to think critically about how and why it’s applied.

For borrowers, recognising this can empower us to question the rates we’re offered, push for fairer lending practices, and make more informed financial decisions.